What Is SST Registration?

Sales and Service Tax (SST) registration is a mandatory requirement for businesses in Malaysia that meet the taxable threshold set by the Royal Malaysian Customs Department (RMCD).

Depending on the nature of the business, companies may be required to register for:

- Sales Tax

- Service Tax

- Or both

Many service-based businesses such as consultants, agencies, professional firms, and digital service providers may fall under Service Tax requirements.

Who Needs to Register for SST?

SST registration may apply to businesses that:

- Provide taxable services

- Sell taxable goods

- Exceed the prescribed taxable threshold

- Operate within taxable business categories determined by RMCD

Common Businesses That May Require SST Registration

- Marketing agencies

- Consultants

- IT & software companies

- Professional service firms

- Event agencies

- Training providers

- E-commerce businesses

- Manufacturers

SST Registration Threshold

| Tax Type | Registration Threshold |

| Service Tax | Generally RM500,000 taxable turnover annually* |

| Sales Tax | Depends on business and taxable goods category |

* Certain industries may have different thresholds depending on regulations.

Registration Requirement

Businesses that exceed the taxable threshold are generally required to register for SST within the prescribed timeline by RMCD.

Failure to register on time may result in penalties and backdated tax liabilities.

What Information Is Required for SST Registration?

SST registration may require:

- Company registration details

- Business activity information

- Revenue information

- Financial records

- Supporting documents from RMCD

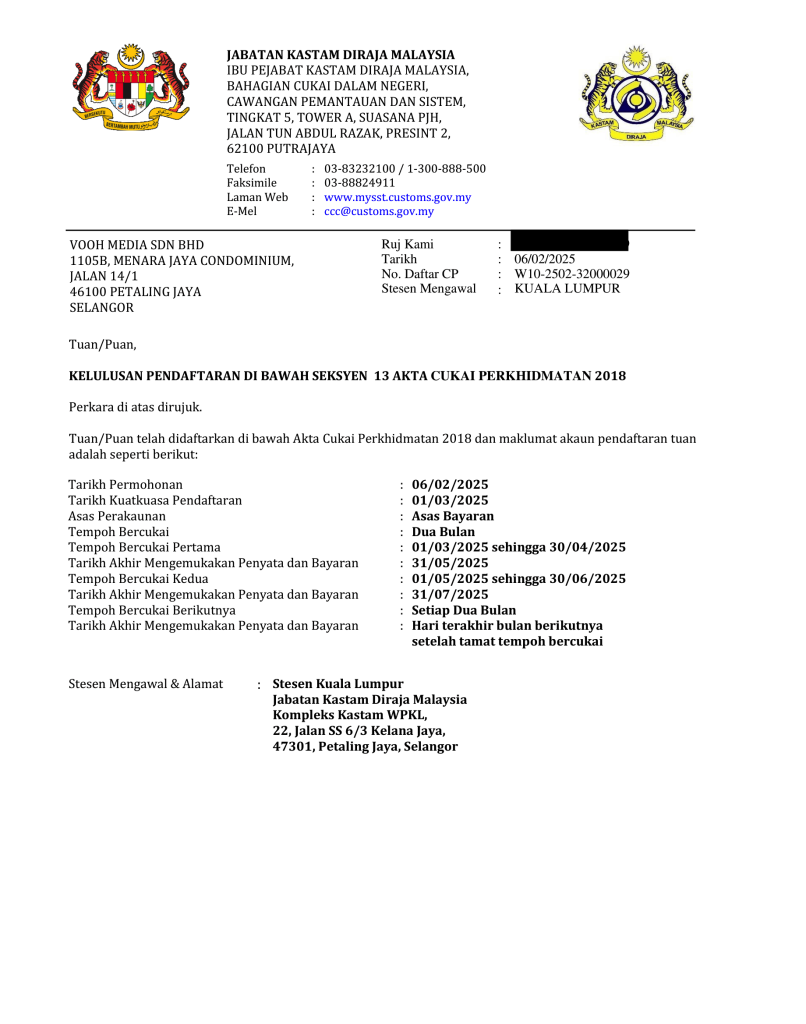

Sample of SST Registration

Consequences of Failing to Register for SST

Businesses that fail to register for SST despite exceeding the threshold may face penalties and enforcement action by RMCD.

Possible Penalties & Consequences

| Offence | Possible Penalty / Consequence |

| Failure to register for SST | Fine of up to RM30,000 |

| Continued non-compliance | Further penalties may apply |

| Failure to charge SST after exceeding threshold | Risk of backdated tax liabilities |

| Failure to comply with SST regulations | Enforcement action by RMCD |

Risk of Backdated SST Payments

One of the biggest risks of late SST registration is:

Businesses may still be required to pay SST retrospectively from the date they should have registered, even if SST was never charged to customers.

This may create:

- unexpected tax liabilities

- cash flow issues

- profit margin losses

- operational disruptions

Important Reminder

Some businesses assume SST only applies to large corporations.

However, many SMEs and service-based businesses may cross the registration threshold without realising it, especially when revenue grows quickly.

Common Mistakes

- Assuming SST does not apply to service businesses

- Monitoring revenue too late

- Confusing SST with income tax

- Delaying registration after exceeding threshold

- Not charging SST after registration becomes mandatory

How Altomate Can Help

Many businesses are unsure:

- whether SST applies to them

- when registration becomes mandatory

- how to monitor taxable turnover properly

Altomate helps simplify the process through:

- SST registration eligibility assessment

- SST registration support

- Revenue threshold monitoring

- Bookkeeping support

- SST filing assistance

- Compliance reminders

- Ongoing tax compliance support

This helps businesses reduce the risk of:

- Late SST registration

- Backdated SST liabilities

- Incorrect SST filings

- Compliance penalties

- Unexpected tax exposure

Need Assistance?

Contact Altomate on WhatsApp for assistance with:

- SST registration

- SST compliance checks

- Revenue threshold assessment

- SST filing support

- Bookkeeping & tax compliance

- Ongoing SST compliance management