What Is Withholding Tax?

Withholding Tax (WHT) is a tax deducted and paid to Lembaga Hasil Dalam Negeri (LHDN) when a Malaysian company makes certain payments to non-residents.

This commonly applies to payments made to:

- overseas service providers

- foreign freelancers or consultants

- non-resident companies

- foreign contractors

- overseas software or digital service providers

The payer is responsible for deducting and remitting the tax to LHDN.

Who Needs to Comply with Withholding Tax?

Withholding Tax obligations may apply to companies in Malaysia that make payments to non-residents for:

- Technical services

- Management services

- Royalties

- Software licenses

- Digital services

- Rental of movable property

- Interest payments

- Contract payments to foreign contractors

Withholding Tax Requirement

| Requirement | Timeline |

| Deduct Withholding Tax from payment | Upon payment or crediting |

| Remit Withholding Tax to LHDN | Within 1 month from payment date |

Example

If payment is made to a non-resident vendor on:

15 May 2026

The Withholding Tax payment should generally be submitted to LHDN by:

14 June 2026

Common Withholding Tax Rates

| Payment Type | Common WHT Rate* |

| Royalties | 10% |

| Technical / management services | 10% |

| Interest | 15% |

| Contract payments to non-resident contractors | Varies |

* Actual rates may vary depending on tax treaties and specific circumstances.

What Information Is Required?

Withholding Tax submissions may require:

- Non-resident payee details

- Nature of payment

- Invoice and payment records

- Supporting agreements/contracts

- Tax calculation details

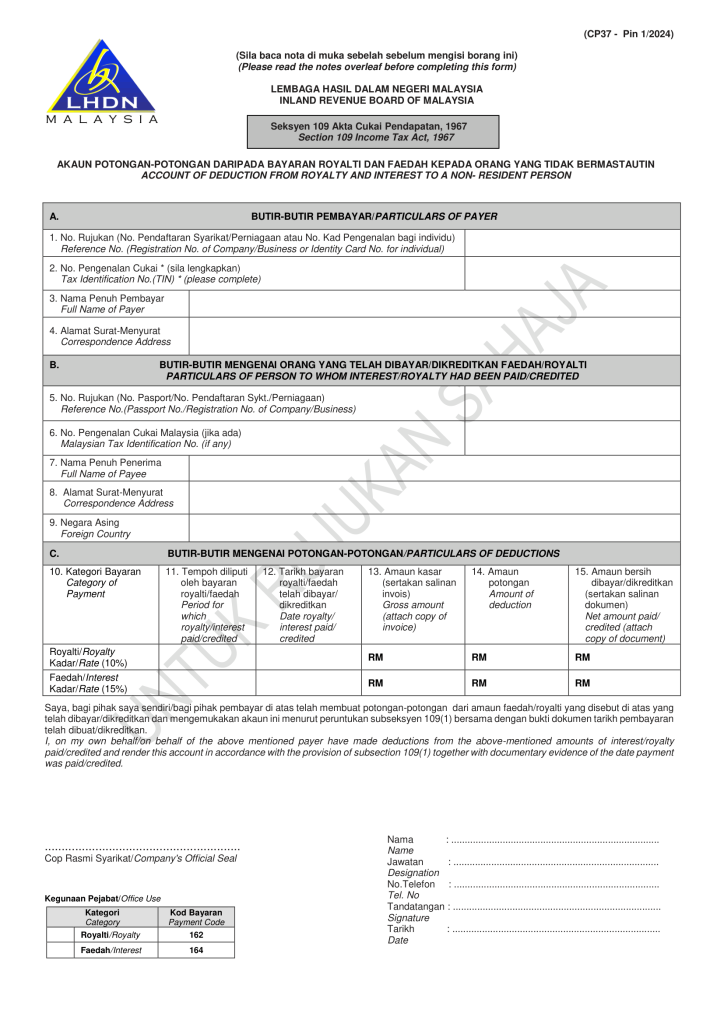

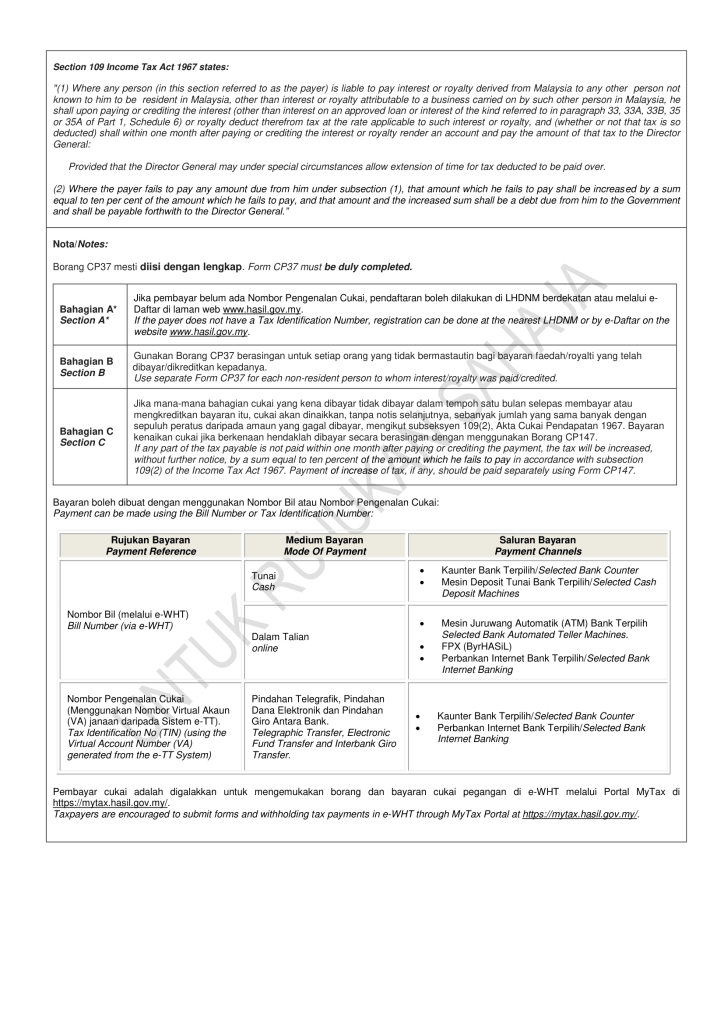

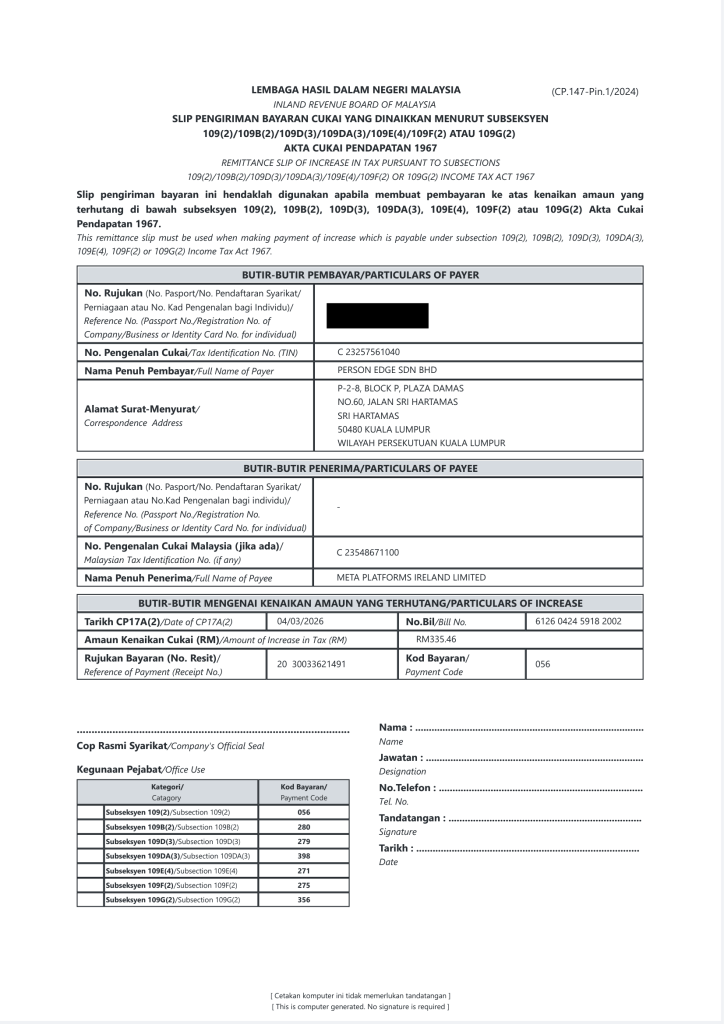

Sample of Withholding Tax Submission

Consequences of Failing to Comply with Withholding Tax

Failure to deduct or remit Withholding Tax may result in penalties and tax exposure under the Income Tax Act 1967.

Possible Penalties & Consequences

| Offence | Possible Penalty / Consequence |

| Failure to remit WHT within required timeline | 10% penalty on unpaid WHT amount |

| Continued non-payment | Additional penalties may apply |

| Failure to deduct WHT from non-resident payment | Company may still be liable for unpaid tax |

| Non-compliance with WHT requirements | Expenses may be disallowed for tax deduction purposes until WHT is paid |

Important Reminder

One of the biggest risks of Withholding Tax non-compliance is:

The related business expense may not be allowed as a tax deduction until the outstanding WHT and penalties are settled.

This may increase:

- taxable income

- corporate tax payable

- overall compliance exposure

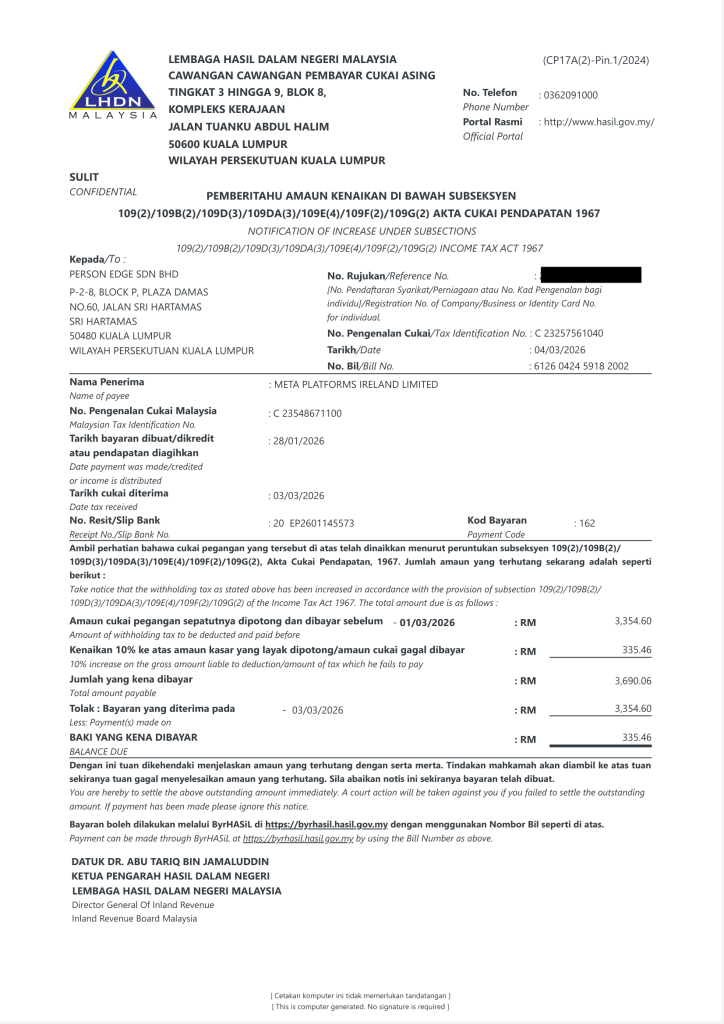

Sample Penalty / Reminder Notice

Common Mistakes

- Assuming overseas payments are automatically tax-free

- Not identifying non-resident transactions properly

- Missing the 1-month remittance deadline

- Ignoring software or digital service payments

- Confusing SST with Withholding Tax obligations

How Altomate Can Help

Withholding Tax compliance can become confusing when companies engage overseas vendors, consultants, or digital service providers.

Many businesses are unsure:

- whether WHT applies

- what tax rate should be used

- whether treaty exemptions are available

- when payment deadlines apply

Altomate helps simplify the process through:

- WHT applicability assessment

- WHT calculation support

- LHDN submission assistance

- Compliance deadline reminders

- Bookkeeping & payment tracking

- Support for overseas vendor transactions

- Ongoing tax compliance guidance

This helps businesses reduce the risk of:

- Late WHT payments

- Tax deduction disallowances

- Incorrect tax calculations

- LHDN penalties

- Unexpected tax liabilities

Need Assistance?

Contact Altomate on WhatsApp for assistance with:

- Withholding Tax compliance

- Overseas payment assessments

- WHT calculations

- LHDN submission support

- Bookkeeping & tax compliance

- Ongoing tax advisory support