What Is CP204?

CP204 is a mandatory tax estimate submission to Lembaga Hasil Dalam Negeri (LHDN) for companies in Malaysia.

It informs LHDN of the estimated tax payable for the current Year of Assessment (YA).

Companies are generally required to estimate and pay their corporate income tax in monthly instalments throughout the year.

Who Needs to Submit CP204?

CP204 is generally required for:

- Sdn Bhd companies

- Active companies generating income

- Companies with taxable business income

Exception

Newly incorporated companies with:

- Paid-up capital of RM2.5 million and below

- Gross business income below RM50 million

may qualify for exemption from CP204 instalment payments for the first 2 Years of Assessment.

Submission Requirement

| Requirement | Timeline |

| Submit CP204 | At least 30 days before the beginning of the basis period |

| New companies | Within 3 months from commencement of operations (if applicable) |

| Monthly tax instalment payment | By the 15th of each month |

Example

If your company’s financial year starts on:

1 January 2026

Your CP204 submission should generally be made by:

1 December 2025

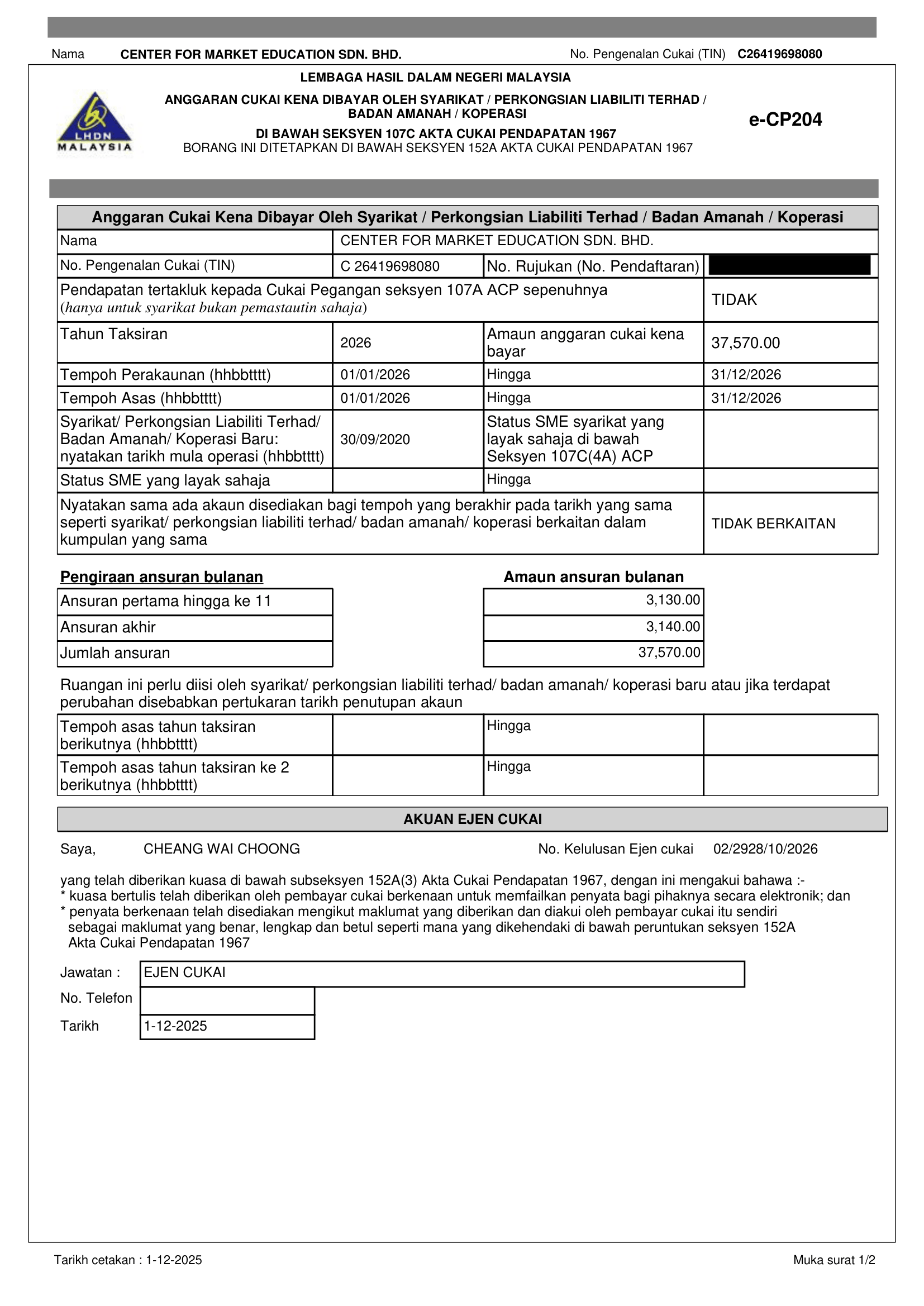

What Information Is Included in CP204?

CP204 typically includes:

- Estimated chargeable income

- Estimated tax payable

- Basis period information

- Company tax reference number

- Instalment schedule

Sample of CP204 Submission

Consequences of Failing to Submit CP204

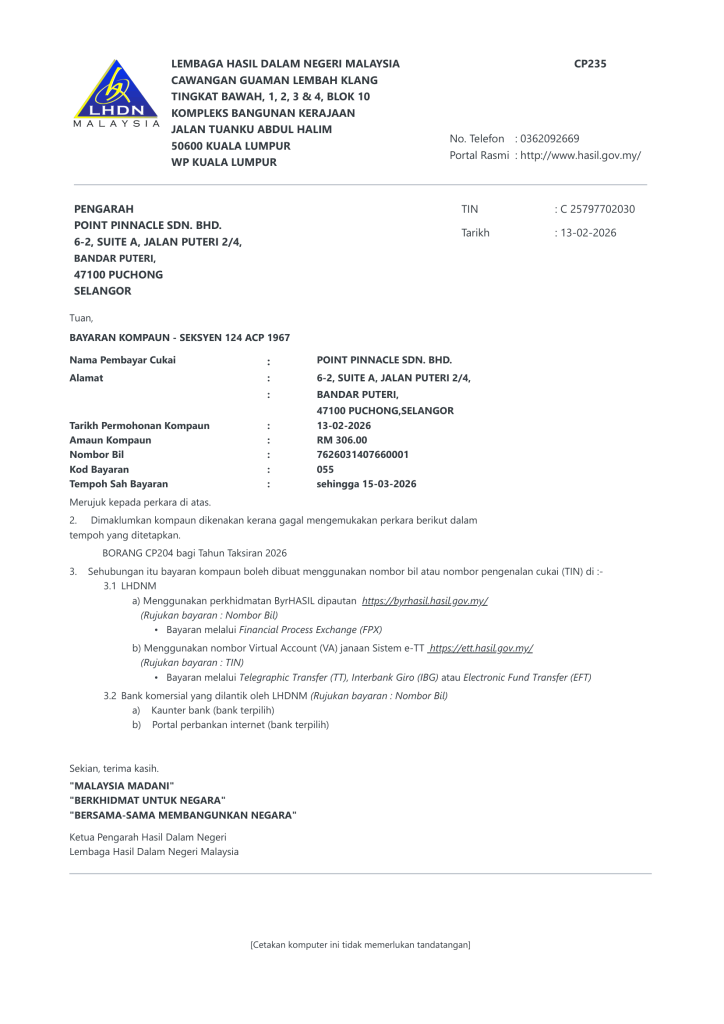

Failure to submit CP204 or pay instalments on time may result in penalties imposed by LHDN.

Possible Penalties & Consequences

| Offence | Possible Penalty / Consequence |

| Failure to furnish CP204 | Penalty may be imposed by LHDN |

| Late payment of monthly tax instalments | 10% increase on unpaid amount |

| Failure to pay increased tax after penalty | Additional 5% increase may apply |

| Significant underestimation of tax payable | Additional penalties may be imposed |

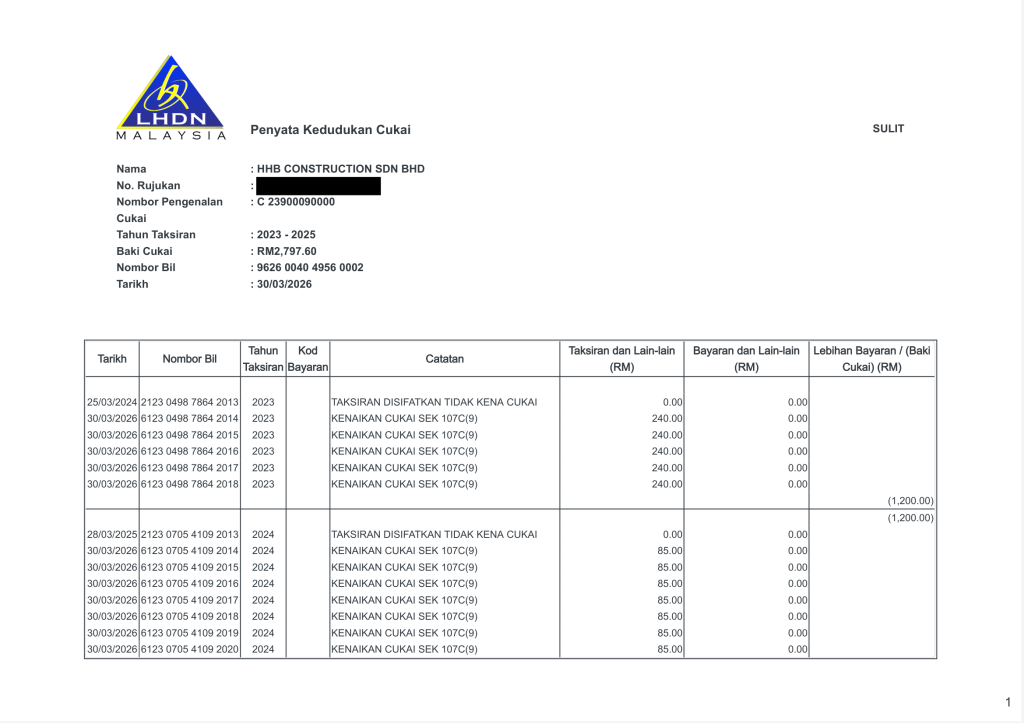

Late Payment Penalties

If monthly tax instalments are not paid by the due date:

- A 10% penalty may be imposed on the unpaid balance

- An additional 5% penalty may apply if the outstanding amount remains unpaid after 60 days

Important Reminder

Submitting CP204 does not replace:

- Corporate tax filing (Form e-C)

- Tax payment obligations

- Accounting record requirements

Companies are still required to maintain proper bookkeeping and tax compliance records.

Sample Penalty / Reminder Notice

Late Payment

Late Filing

Common Mistakes

- Forgetting to submit CP204 before the deadline

- Underestimating taxable income too aggressively

- Missing monthly instalment payments

- Assuming dormant status automatically grants exemption

- Confusing CP204 with annual tax filing

How Altomate Can Help

Managing CP204 can be confusing, especially for new business owners who are unsure:

- whether their company is exempt

- how much tax to estimate

- how to avoid underestimation penalties

- when instalment payments are due

Altomate helps simplify the process through:

- CP204 eligibility assessment

- CP204 preparation & submission

- Estimated tax calculations

- Monthly instalment reminders

- Tax estimate revisions (CP204A)

- Bookkeeping support for better tax forecasting

- Corporate tax compliance support

This helps businesses reduce the risk of:

- late submissions

- missed instalment payments

- inaccurate tax estimates

- unnecessary penalties from LHDN

Need Assistance?

Contact Altomate on WhatsApp for help with:

- CP204 submissions

- Tax estimate revisions

- Late payment guidance

- Corporate tax compliance

- Ongoing bookkeeping & tax support